Overview

February brought a mix of performance across global markets, with U.S. equities experiencing declines after a strong start to the year. The S&P 500 and Russell 3000 indexes faced losses, driven largely by underperformance in tech stocks, while large and mid cap stocks outpaced small caps.

In contrast, defensive sectors such as consumer staples and utilities performed well. International equities showed resilience, with European markets, particularly Germany, seeing notable gains, while Japan lagged. Emerging markets (EM) were mixed, with China posting strong returns and India and Taiwan facing challenges.

In fixed income, lower yields across the curve provided a safe haven, leading to gains in longer-duration assets, including Treasuries and corporate bonds.

Real assets also outpaced broader markets, with U.S. REITs benefiting from lower yields and increased deal-making activity. Energy commodities saw a boost from cold weather, though crude oil prices faced pressure. Overall, February highlighted a tug-of-war between risk sentiment and defensive positioning in the face of economic uncertainties.

Equities

After a positive start to the year in January, domestic equity markets fell in February. The S&P 500 declined 1.3% and the broader Russell 3000 Index lost 1.9% for the month. Large and mid cap stocks outpaced small caps, with the Russell 1000 Index gaining 1.7% versus 5.3% for the Russell 2000 Index. After trailing sharply in 2024, value stocks outperformed their growth counterparts for the second consecutive month; the Russell 3000 Value Index eked out a 0.2% gain vs. a 3.7% loss for the Russell 3000 Growth.

Five of the “Magnificent 7” stocks lagged the broad market in the sell-off, with only NVIDIA (+4.0%) and Apple (+2.6%) posting gains for the month. Tesla (−27.6%), Amazon (−10.7%), and Alphabet (−16.5%) were the three largest individual detractors. Consumer discretionary (−8.9%) and communications services (−6.2%) were the two worst performing sectors in February. On the other hand, defensive sectors protected investors’ capital in a risk-off environment, with consumer staples (+5.0%), real estate (+3.7%), and utilities (+2.0%) all finishing in the positive territory. Energy (+2.6%), a laggard in the prior 12 months, also posted a modest gain.

Overseas equities remained surprisingly strong, with both developed (+1.9%) and emerging (+0.5%) markets rising for the month and outpacing U.S. equities. Europe (+3.7%) experienced a reversal in performance as investor inflows increased, the threat of tariffs had yet to materialize, and efforts were made toward peace in Ukraine. Germany (+3.9%), much maligned in 2024 due to economic malaise and political turmoil, has been a standout in 2025 due to hopes it will loosen fiscal policy. Japan was an exception, with the Nikkei 225 down 6% in February. However, these losses were muted for U.S.-based investors because of the 2.8% rise of the yen vs. the U.S. dollar (USD).

Mixed performance across EM countries masked a noteworthy recovery in China (+11.8%). While economic and geopolitical uncertainty remain heightened, enthusiasm around DeepSeek’s lower cost AI-model helped reignite excitement around China’s tech prospects and drove a rally in MSCI EM Index giants such as Alibaba (+44.7%) and Tencent (+19.5%). A meeting between Chinese President Xi Jinping and several of the country’s top corporate executives also lifted optimism. The meeting signaled a turnaround in Beijing’s approach toward private sectors—notably tech—following years of regulatory assault. A reversal in India (−8.1%), which continues to battle slower economic growth, and tech-heavy markets such as Taiwan (−4.4%) offset these gains. Despite continued strong demand for its high-end chips, Taiwan Semiconductor (−8.6%), which represents over 50% of the MSCI Taiwan Index, was pulled down on profitability concerns as the company seeks to diversify its global supply chains.

Fixed Income

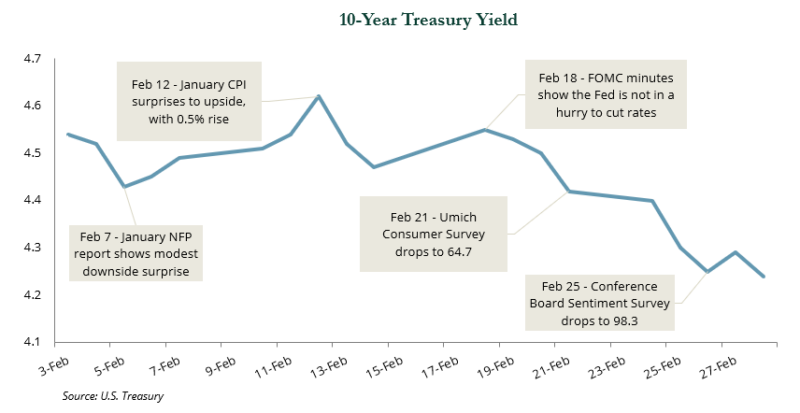

In February, as risk assets sold off amid mounting growth concerns, fixed income served as a safe haven. The asset class broadly delivered positive returns as yields fell sharply across the curve and provided a boost to performance. However, the path lower was volatile, as rates fluctuated throughout the month on economic news.

Early on, yields climbed following hotter-than-expected CPI data, but eventually retreated as growth fears took hold and consumer confidence waned—as illustrated by the sharp monthly decline in the February Conference Board Consumer Confidence Survey.

By month-end, the 10-year yield stood at 4.19%, down 36 bps, while the 2-year yield fell 22 bps to 3.98%.

The sharp decline in yields fueled sizable gains across core fixed income sectors, with longer duration assets leading the way. Long duration Treasuries surged 5.2%, easily outpacing returns of 2.4% for intermediate Treasuries and 0.7% for short Treasuries.

Meanwhile, U.S. mortgage-backed securities and investment grade corporates posted returns of 2.6% and 2.0%, respectively, contributing to a 2.2% gain for the Bloomberg Aggregate Index. The fall in Treasury yields did cause some spread widening in leveraged credits, but the additional carry in high yield and leveraged loans allowed these sectors to deliver positive returns of 0.7% and 0.1%, respectively.

Real Assets

Real assets generally outpaced broader markets in February. Global REITs were up 2.2%, led by U.S. REITs (+3.7%), which rose on a drop in 10-year Treasury yields, increased deal making activity, and greater debt availability. The healthcare (+9.4%) and telecom REITs (+9.5%) sectors—which have compelling demand outlooks and posted strong fourth quarter results—led the way, while office (−3.9%) and lodging REITs (−5.2%) were down. Clean energy (−2.2%) was down on policy uncertainty, while global infrastructure (+0.1%) and metals and mining equities (+0.1%) were slightly positive.

Cold weather helped to push natural gas prices (+30.9%) higher and demand continued to increase from data centers and the electrification of the economy. Natural gas prices, which are sensitive to short-term weather events, were up 138.2% year-over-year. WTI crude prices dropped 3.8% following OPEC+’s decision to begin unwinding voluntary production cuts starting in April. Crude prices were also negatively affected by rising U.S. inventories and fears of a tariff-induced economic slowdown. North American natural resource equities (+1.4%) ended the month in positive territory. MLPs (+3.4%) continued to benefit from growing power demand, rising natural gas prices and attractive relative dividend yields. Commodities were up 0.8%, led by the energy subindex (+4.9%), as the agriculture (−2.3%) and livestock (−5.4%) subindexes fell on concerns over the impending trade war. ⬛

Indices referenced are unmanaged and cannot be invested in directly. Index returns do not reflect any investment management fees or transaction expenses. Copyright MSCI 2025. Unpublished. All Rights Reserved. This information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an “as is” basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any other person involved in or related to compiling, computing or creating this information makes any express or implied warranties or representations with respect to such information or the results to be obtained by the use thereof, and MSCI, its affiliates and ech such other person hereby expressly disclaim all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any other person involved in or related to compiling, computing or creating this information have any liability for any direct, indirect, special, incidental, punitive, consequential or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have anticipated, the possibility of such damages. Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, it shall not have any liability or responsibility for injury or damages arising in connection therewith. Copyright ©2025, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact. FTSE International Limited (“FTSE”) © FTSE 2023. FTSE® is a trade mark of the London Stock Exchange Group companies and is used by FTSE under license. All rights in the FTSE indices and / or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. Indices referenced are unmanaged and cannot be invested in directly. All commentary contained within is the opinion of Prime Buchholz and is intended for informational purposes only; it does not constitute an offer, nor does it invite anyone to make an offer, to buy or sell securities. The content of this report is current as of the date indicated and is subject to change without notice. It does not take into account the specific investment objectives, financial situations, or needs of individual or institutional investors. Some statements in this report that are not historical facts are forward-looking statements based on current expectations of future events and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. Information obtained from third-party sources is believed to be reliable; however, the accuracy of the data is not guaranteed and may not have been independently verified. Performance returns are provided by third-party data sources. Past performance is not an indication of future results. Prime Buchholz LLC© 2025