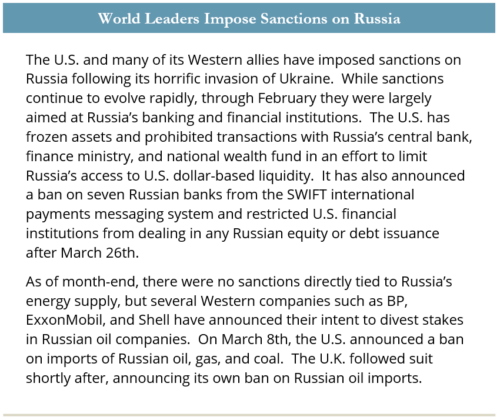

Russia’s invasion of Ukraine dominated headlines and capital markets during February. Even before the month started, investors were concerned about elevated geopolitical risk and the potential impact on inflationary pressures around the globe. Unfortunately, the worst case scenario materialized, with Russia launching a full scale war on February 24th.

Markets reacted by going into risk-off mode, with volatility spiking, gold strengthening, and equities coming under pressure. However, the most significant market impact was in the energy space, as we outlined in our recent investment perspective, Markets React to Russia’s Invasion of Ukraine. Oil prices, which were already up 14.8% in January, rose another 9.8% in February. The Brent crude oil futures curve moved to steep backwardation, indicating the near-term market for crude is exceptionally tight.

Natural gas prices, which remain largely regional in pricing despite steps toward global integration, spiked by as much as 40% during the month and finished up 17% (U.K. spot price). Russia supplies approximately 40% of Europe’s natural gas and historically has been the continent’s cheapest and most reliable supplier. Flows of gas to Europe continued unabated during February, but the potential for disruption due to sanctions by Russia, the West, or from the conflict itself remain a distinct possibility.

Although energy only accounts for approximately 7.3% of the CPI, higher energy costs impact (on a lagged basis) other CPI categories, including transportation, clothing, apparel, and food and beverages. With CPI at 7.5% at the end of January—well above the Fed’s 2% target—elevated energy prices could potentially exacerbate inflationary pressures.

Other commodity prices also increased, including agricultural commodities (+8.9%), precious metals (+6.5%), and industrial metals (+6.4%). As a safe haven, gold gained 5.8%. Food prices are a potential concern, as fertilizers use large amounts of natural gas and Russia and Ukraine account for approximately 25% of global grain exports. Further, Russia produces just under 50% of the world’s palladium and both countries export smaller amounts of other metals (platinum, nickel, aluminum, steel). Disruptions to supply for a range of these commodities as a result of the conflict, sanctions, or Russian countermeasures would likely have an inflationary impact across the West.

Other commodity prices also increased, including agricultural commodities (+8.9%), precious metals (+6.5%), and industrial metals (+6.4%). As a safe haven, gold gained 5.8%. Food prices are a potential concern, as fertilizers use large amounts of natural gas and Russia and Ukraine account for approximately 25% of global grain exports. Further, Russia produces just under 50% of the world’s palladium and both countries export smaller amounts of other metals (platinum, nickel, aluminum, steel). Disruptions to supply for a range of these commodities as a result of the conflict, sanctions, or Russian countermeasures would likely have an inflationary impact across the West.

Breakeven rates on 5- and 10-year TIPS increased 30 and 20 bps, respectively, indicating higher market inflation expectations. Investors are pricing in a 25 bps rate hike for the March Fed meeting and the likelihood that the federal funds rate could be in the 1.50–1.75% range by year end. Investors are closely monitoring the Fed’s expectations, particularly in light of the potential economic impact of Russia’s actions, sanctions, and rising commodity prices.

February saw continued upward movement in interest rates as the expectation for interest rate hikes and higher inflation continued to mount. While rates rose across the U.S. Treasury curve, the increases were most pronounced at the short end. For the month, 2-year Treasuries rose 27 bps to 1.43%; the curve flattened as a result, with the 2s-10s spread (the difference between the 10-year and 2-year Treasury yields) falling 21 bps to 41 bps. Rising yields, along with wider spreads, resulted in negative total returns for U.S. corporate debt; the broad Bloomberg U.S. Corporate Index was down 2.0% on the month. Investment grade corporate credit option-adjusted spreads are at the widest level since October 2020.

REITs declined along with broader markets during February (−2.4%) and year to date (−8.0%). However, this follows 2021, when REITs outperformed all other sectors—with the exception of energy—as inflation emerged as a concern. Historically, REITs have performed well during rate hiking cycles and have provided an inflation hedge due to their ability to pass along higher costs via rent adjustments, increasing barriers to entry (i.e., zoning and environmental restrictions), and higher replacement costs (costs to construct new supply) in an inflationary environment.

Equity markets sold off for the second consecutive month amid an uptick in volatility, with the VIX Index rising from 24.8 at the end of January to 30.2 in February. Higher yields put pressure on long duration names in IT and communication services sectors while resource equities performed well amid higher commodity prices. As a result, value stocks outpaced their growth counterparts across all regions.

The MSCI Emerging Markets Index (−3.0%) was weighed down by Russia, where markets fell 52.8%. Russia’s domestic equity market closed on the last trading day of the month with no immediate prospects of reopening. Further, the Russian central bank banned overseas institutions from selling local securities on the Moscow Exchange. Shortly after the month-end, MSCI, FTSE Russell, and other index providers announced they would delete Russian securities from indices. Negative sentiment weighed on emerging markets broadly and dragged down China (−3.9%) and Taiwan (−2.6%). A large commodity importer, India (−4.0%) was also pressured by rising prices in the sector.

Developed equities also posted a drawdown, with the MSCI EAFE Index selling off 1.8% for the month. The Index was buoyed by strong performance from resource-rich geographies such as Australia (+6.0%) and Norway (+4.2%). The worst performing countries were Austria (−15.0%) and Sweden (−8.1%), which sold off on geopolitical risk concerns.

The S&P 500 (−3.0%) entered its first correction since the start of the pandemic. The broader Russell 3000 Index performed slightly better with a 2.5% drawdown. In a sharp trend reversal, small caps outpaced large caps, with the Russell 2000 Index gaining 1.1% versus a 2.7% drawdown for the Russell 1000 Index. Prior to February, small caps had lagged large caps in 10 of the past 11 months.

Energy (+7.5%) was the best performing sector within the Russell 3000 for the second consecutive month. Materials (+1.8%) was the only other sector to finish in positive territory on the strength of metals and mining stocks. Industrials (−0.6%) posted a modest drawdown, buoyed by strong performance from defense contractors such as Raytheon Technologies (+14.3%) and Lockheed Martin (+12.0%). Communications services (−6.7%) was the worst performing sector, hindered by the weakness in Meta Platforms (−32.6%). The Meta sell-off resulted in the largest ever one-day shareholder value destruction ($250+ billion) by a single company, as the social media platform struggled with Apple’s privacy changes and competition from TikTok. Information technology (−4.5%) was the second worst performing sector amid pullbacks from blue chips Apple (−5.4%) and Microsoft (−3.8%).