The year 2020 will be remembered as one of the most challenging in human history. Before we begin our review of the financial markets, we need to acknowledge the previously unimaginable impact of the virus. COVID-19 has infected more than 88 million people in 191 countries, which has led to the deaths of nearly 2 million people worldwide. The impact on families, businesses, industries, and governments has been far-reaching and a recovery will take years in many cases.

Throughout the pandemic, we have been inspired by the efforts of health care professionals, medical researchers, and front-line workers. The dedication of these individuals gives us hope, and highlights what can be achieved when we work together. We remain hopeful and committed to the continuing efforts of working to achieve the investment objectives of our incredible clients.

This unprecedented period of challenges and strife began in the early days of the new year. The virus quickly spread around the globe and the first known case in the U.S. was recorded on January 19th. With so much uncertainty surrounding the nature of the virus, the initial government response was limited and involved simple guidance like washing hands and social distancing. As infection rates soared, the probability of a nationwide shutdown like what had been implemented in Europe and some Asia-Pacific countries increased, causing considerable market volatility and meaningful declines across asset classes.

Policymakers responded with the Federal Reserve cutting interest rates to zero, launching an unparalleled quantitative easing program, and expanding the scope of the post-Global Financial Crisis lending programs. With a large equity infusion by the U.S. Department of the Treasury as a backstop, the Fed had trillions of dollars available to lend, expand the purchase of assets to include corporate bonds and ETFs, and ensure the financial system was awash in liquidity. Congress quickly enacted two stimulus measures—one of which was the record $2.3 trillion CARES Act—before brinkmanship slowed progress on a third package. Ultimately, a third stimulus package of $900 billion was enacted as the year came to a close.

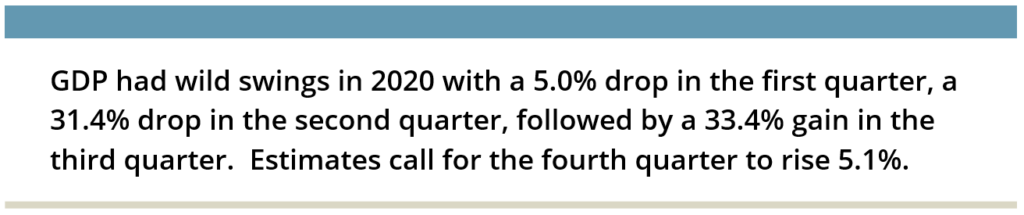

With extraordinary monetary and fiscal response, markets rallied at the end of March and through the end of the year. Markets set records that included the economy’s sharpest drop (second quarter) and sharpest recovery (third quarter). The S&P fell into bear market territory over a 22-day period before reaching all-time highs as the year progressed. With positive developments around a vaccine, optimism remained strong as 2020 came to a close.

Among equity markets, the U.S. was once again the best performing region, with the Russell 3000 Index gaining 20.9% in 2020. The strong calendar year performance masked a sharp drawdown in the first quarter, followed by an even sharper snapback. The Index declined 35.0% from February 19th through March 23rd, and saw the 11-year bull market come to a remarkable and swift end. Equities entered bear market territory over the fewest number of trading days dating back to the Great Depression. However, the Index roared back 76.8% since March 23rd, aided by strong fiscal and monetary stimulus and positive vaccine trials.

Consumer discretionary (+46.9%) was the best performing sector of the index, propelled by outsized gains from Amazon (+76.3%) and Tesla (+743.4%). While Tesla had been a longstanding member of the Russell 3000 Index, when it was added to the S&P 500 in December it was the sixth largest constituent of the S&P 500, just below Facebook and above Berkshire Hathaway. IT (+46.2%) stocks also posted very strong gains, as the pandemic pulled forward demand for IT products and services. On the other end of the spectrum, energy (−33.2%) was by far the worst performing sector amid a sharp decline in oil prices. Real estate (−4.6%) and financials (−2.2%) were the only other GICS sectors to finish the year in negative territory.

The strong performance from the IT and consumer sectors, along with drawdowns from energy and financials, resulted in a banner year for growth stocks relative to value stocks. The Russell 3000 Growth Index gained 38.3% compared to a 2.9% advance for the Russell 3000 Value Index on the year—the largest ever calendar year spread between the style indices. Similar dynamics were observed abroad, where the MSCI EAFE Growth and MSCI EM Growth Indexes outpaced their value counterparts by 2,090 bps and 2,580 bps, respectively.

Large caps edged out small caps for the year, with the Russell 1000 Index gaining 21.0% and the Russell 2000 Index advancing 20.0%. Large caps sharply outperformed small caps through August, but market leadership reversed for the final four months of the year in the wake of optimism for the vaccine. In November, when the first successful vaccine trials were announced, the Russell 2000 Index posted its best month ever with an 18.4% gain.

Non-U.S. equities also ended a tumultuous year with strong gains. The MSCI EAFE Index was in the red for much of 2020, but a fourth quarter rally (+16.1%) propelled the benchmark to a 7.8% return. The late rally was driven by a reversal in style leadership, as well as a long-awaited resolution to Brexit as the U.K. and European Union struck a trade

agreement just before year-end. Despite the strong close, developed non-U.S. equities lagged well behind their domestic counterparts. The disparity was due in large part to the differing composition of each market. Tech and e-commerce names were more resilient as the pandemic brought forth lockdown measures and social restrictions. Tech names rose 28.4% in the MSCI EAFE Index, but accounted for less than 9% of the Index compared to more than 25% for the Russell 3000 Index. Developed non-U.S. markets also lacked exposure to the kinds of large internet and e-commerce companies that are more prominent in the U.S. and emerging markets (EM). The MSCI EAFE instead is more diversified and holds greater exposure to areas like industrials, consumer staples, and health care.

The strength of tech/internet companies like Tencent (+51.3%), Taiwan Semiconductor Manufacturing (+75.8%), and Samsung Electronics (+58.4%) buoyed EM equities, which gained 18.3%. Country returns in the EM space varied widely. Countries that were most effective in combatting the pandemic, such as Korea (+44.6%), Taiwan (+41.0%), and China (+29.5%), were among the best performing countries in the world. Those that applied a less robust public health response and/or suffered from widespread COVID-19 cases were among the worst performers. Latin American countries such as Brazil (−19.0%) and Colombia (−19.0%) were particularly hard hit.

U.S. Treasuries responded to Fed actions as the sharp reduction in the federal funds rate caused the front-end of the yield curve (the 3-month T-bill out to the two-year note) to fall close to the zero lower bound. Along the intermediate and long-term portions of the curve, the combination of the Fed’s quantitative program and investor demand for safe haven assets caused yields to fall despite a heavier supply of Treasuries to finance the deficit. However, this was by a smaller magnitude than the drop in the front-end of the curve. Even though the curve steepened, long Treasuries rallied 17.6% in 2020 and outpaced the 9.0% gain in intermediate-term Treasuries and the 3.1% rise in short-term Treasuries.

After meaningfully widening at the outset of the pandemic, credit spreads narrowed after monetary and fiscal measures restored optimism. However, credit spreads did not fully retrace the widening that occurred through late March and ended the year modestly higher than levels at the end of 2019. High yield spreads were 360 bps over comparable Treasuries at the end of 2020, up from 336 bps at the end of 2019. Investment-grade corporate spreads ended 2020 at 96 bps, 3 bps higher than 2019. However, falling absolute yields had a more profound impact on performance than spread movements, helping investment-grade corporates rise 9.8% in 2020 and high yield to gain 7.1%. With the aid of Fed buying programs and fears of a heightened default cycle, investment-grade outperformed high yield credit.

Many of the same themes that played through the equity markets held true for long/short equity hedge funds. Growth-oriented managers outperformed their value peers and many tech-focused strategies reported returns well in excess of the broader market. Dispersion amongst managers was considerable as a result. Strong performance was largely driven by security selection on the long side of portfolios, with big tech and payment-oriented companies such as Visa, MasterCard, and PayPal among the more widely held top performers. Short portfolios and hedging programs were put to the test in the first quarter and managers that were able to pivot to a longer-biased stance over the rest of the year fared well. Those that stayed hedged struggled to keep up as the markets rallied. The frequent changes in market leadership—most notably the defensiveness of technology in February/March and rally in high beta stocks following the election in November—wreaked havoc on quantitative equity strategies, with many posting sizable losses on the year.

Absolute return manager performance was also disparate. Managers with robust hedging programs protected capital in the first quarter, while more directional distressed managers struggled as already-troubled companies in the midst of a restructuring had to contend with a global economic shutdown. Distressed managers were also quick to launch drawdown funds in an effort to take advantage of opportunities created by the pandemic. Top performing credit managers took advantage of the market weakness in March to add exposure to investment-grade and high yield credit trading at steep discounts to par. Managers harvested gains on those positions in the back half of the year, with many anticipating an uptick in defaults and new distressed opportunities entering 2021. Merger volumes were relatively low, limiting arbitrage opportunities. However, issuance of special purpose acquisition companies (SPACs) surged in 2020, creating many new arbitrage-like opportunities for event-driven managers.

While breakeven inflation rates (the difference between the nominal yield on U.S. Treasuries and the real yield on U.S. TIPS) widened and optimism remained high, the rally in risk assets did not have a “reflation trade” feel. Many segments within real assets were severely impacted by virus containment measures and there was wide dispersion amongst sub-sectors.

Property stocks fell 8.2% overall, but there was massive dispersion within sectors as new economy sectors generally outperformed traditional segments such as office, hotels, and retail, which were hardest hit by COVID-19. Data centers and industrial were up 19% and 11% on the year, while lodging and office were down 19% and 25%, respectively. When news of vaccine trials hit in November, sector performance sharply reversed as investors sought to gain exposure to a recovery.

Crude oil and natural resource equities finished down 20.5% and 19.0%, respectively. The shuttering of economies in the spring caused crude prices to experience unprecedented declines. Prices traded briefly in negative territory during late April, only to stage a robust recovery and close the year at $50 per barrel as the Organization of the Petroleum Exporting Countries made unprecedented production cuts, demand improved, and positive vaccines news emerged. Global crude demand recovered to 90 million barrels per day to end the year, or approximately 90% of demand for 2019. A full recovery to 2019 levels likely hinges on a recovery in air travel.

Infrastructure securities fared better than traditional resources, declining 5.8% as weaker performance from the midstream energy and transportation sectors was materially offset by strong relative performance from utilities, which were leaders in renewable energy production.

Clean energy indices had a record year, advancing 140%. The universe of investable pure-play public clean energy stocks is concentrated at approximately 30 names, consisting primarily of renewable technology companies (which sharply outperformed during 2020), component manufacturers, developers, and clean energy utilities (production). Some of the largest renewable production owners were conglomerates (including Berkshire Hathaway), traditional utilities, or energy companies. This included Next Era, which has a large asset base split primarily between natural gas and renewable power plants. Broadly defined, the sector continued to benefit from declining costs, as well as government mandates and corporate sustainability initiatives.

Amid this backdrop, the traditional 70/30 portfolio —70% domestic equities (S&P 500)/30% fixed income (Bloomberg Barclays Aggregate)—rose 15.7% in 2020. This mix outpaced the 11.0% increase of a more broadly diversified portfolio, which incorporates non-U.S. developed and EM equities, private equity, real assets, hedge funds, and non-U.S. bonds. Diversified portfolios were hurt by international developed market equities, which lagged U.S. equities by 1,060 bps, and from weak real asset categories like natural resource stocks (−19.0%), real estate (−8.2%), and commodities (−3.1%). Generally, hedge funds protected capital relative to the broad equity market declines during the first quarter and those that were able to nimbly remove short hedges as markets started to rally did well. Traditional hedges, such as U.S. Treasuries, U.S. TIPS, and non-U.S. sovereign debt, posted low double-digit to high-teens returns and outperformed the Bloomberg Barclays U.S. Aggregate Index. While year-end marks are not yet available, early indications are that private capital investments will be additive for diversified structures in aggregate. Venture capital and tech-related investments continue to experience strong performance and robust activity in 2020.

Outlook

There are few things that capital markets dislike more than uncertainty. We have gained clarity on several important issues since 2020 came to an end; however, there are many unknowns that will impact investor portfolios in 2021. Even though the presidential election has passed, the potential for further unrest has not. The shift of power in the oval office and Congress means significant policy changes are likely on the horizon in 2021. Meanwhile, the presence of COVID-19 vaccines has created some optimism, but many questions remain related to the production, distribution, and roll-out. And while capital markets have been willing to look past the immediate economic impact of the pandemic and resultant economic shutdowns, the unprecedented stimulus programs could have significant intermediate- to long-term impacts.

Uncertainty remains, and—as we have seen time and time again—uncertainty leads to volatility. It is crucial to remember that even though it can be uncomfortable, volatility also creates opportunities. We work with each of our clients to create a plan. Executing on that plan when markets are volatile should increase the likelihood of long-term investment program success.